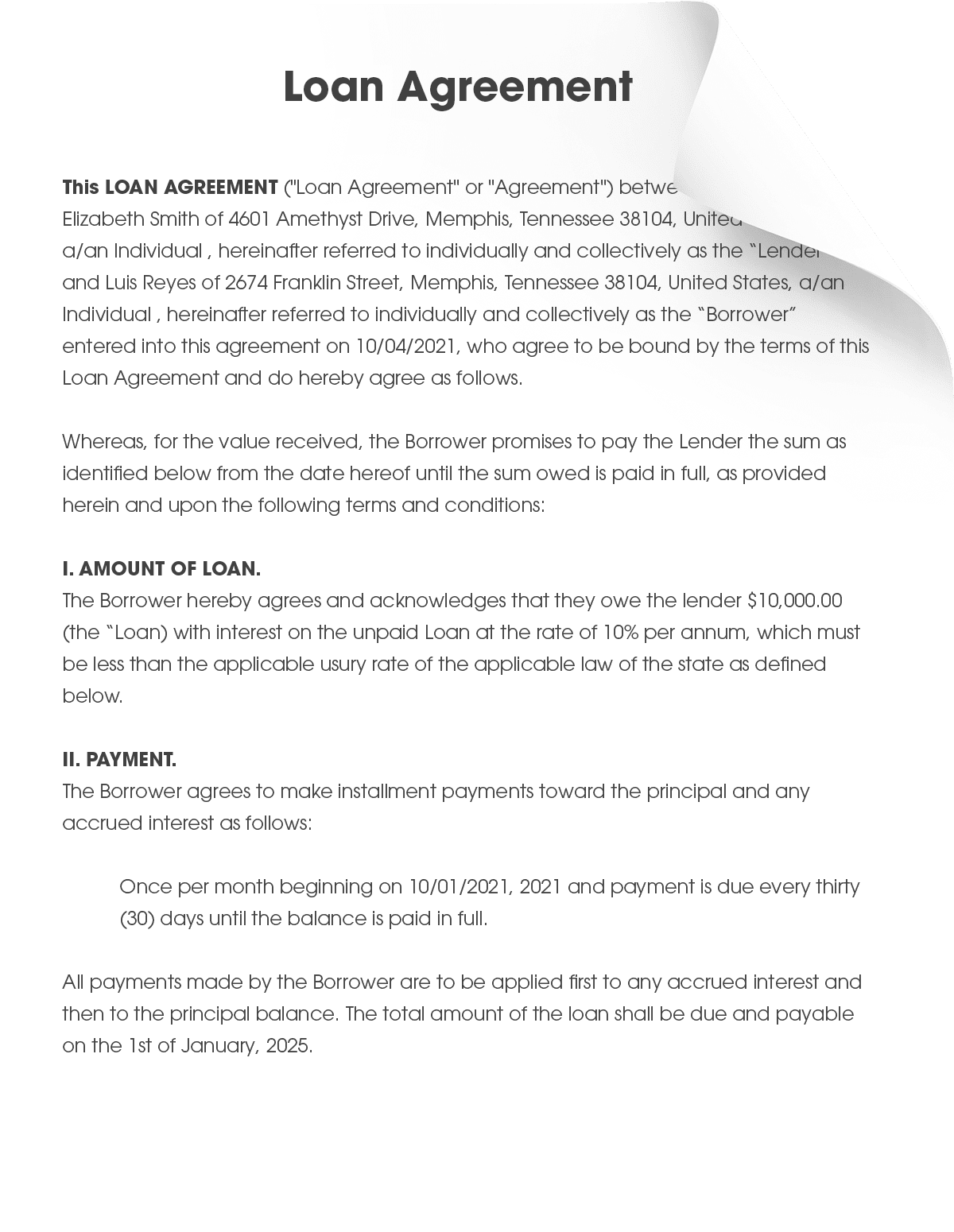

What is a Loan Agreement?

A loan agreement is a document that summarizes the agreement that a borrower and lender have about a loan that is to be repaid. It can help create evidence of your agreement and be used to collect on the loan if the borrower defaults on repayment. The loan agreement includes the amount of money that is being loaned as well as establishing a payment schedule. Loan agreements can be used for various reasons, including a business loan, real estate loans, student loans, personal loans, and many more.

Why do you need to use a Loan Agreement?

You should have a loan agreement if you lend someone you know money and expect to be repaid. A loan agreement sets forth the terms of the contract between both the borrower and the lender. It specifies the loan amount, what the loan is for, and the payment schedule. The agreement protects the lender in the event the borrower defaults. The loan agreement will implement a clear payment schedule that both parties are bound to.

When do you need to use a Loan Agreement?

A loan agreement can be used for many transactions. It can be utilized in a formal setting, such as a real estate purchase, or for an informal loan between family members.

How can having a written loan agreement help me?

Having a written loan agreement can do the following:

- Make sure you are on the same page. Having a written agreement can help the lender and borrower have a clear understanding about the lending and repayment of money. This can help avoid confusion and conflict. If a court has to determine your agreement, it will be much easier when you have a document that clearly spells out the terms of your agreement.

- Make collecting the loan easier. A lender’s written agreement can describe their rights in case the borrower defaults, such as charging late fees or accelerating the loan. The court can only impose those penalties that are provided in your agreement.

- Pay for expenses. If it becomes necessary for lender to pursue collection on the loan, a written agreement can instruct that the borrower has to reimburse lender for collection or enforcement costs.

Are there any deadlines or times when this form is needed?

A loan agreement should be drafted and agreed upon before the commencement of the loan. This protects the parties from any issue that should arise or discrepancies like what was discussed outside of the contract. It also allows the borrower(s) to review and agree to the repayment schedule and inquire about any interest that may be imposed.

Do I need to file my loan agreement anywhere?

No. However, you should keep the original loan agreement with your signature for your records and in case you ever need to present it to the court.

Do I have to charge interest?

Some states may require you to charge interest on a loan. Additionally, not charging interest or charging interest that is less than the applicable federal rate (AFR) can cause negative tax effects to yourself

What information should be in my Loan Agreement?

Your loan agreement should include the following information, at a minimum:

- Borrower’s name

- Borrower’s address

- Lender’s name

- Lender’s address

- The amount of money that is borrowed

- The percentage rate of interest to be charged

- The state whose law will govern the agreement

- The term of the loan

- The frequency of payments on the loan

- The method of how loan payments will be paid

What are the most common mistakes to avoid?

Be sure to include a payment schedule that you can manage. Evaluate the borrower(s) earnings and determine what they could handle as far as a payment plan. For example, sometimes, it is easier for a party to pay weekly instead of monthly. This will all depend on each borrower’s financial situation and the lender’s preferences.

If the lender decides to include any form of interest in the loan agreement, it is critical that they are familiar with their state’s usury laws. The interest rate is a fee paid by the borrower, which is a percentage of the principal amount borrowed. It is a form of security for the lender to take a risk as to providing a loan. Usury laws vary from state to state. They establish the maximum interest rate a lender can charge. The lender should not charge more than is authorized under the applicable law.

Do I need to use a lawyer, accountant or notary public to help me?

Assistance from professionals can ensure that you have a clear understanding of the transaction and your legal rights. A notary public can help verify the signature of the other party. An accountant can discuss how the transaction may affect you or describe potential tax consequences. A lawyer can explain special rules that apply to your state. We’ve got you covered, our experts created a loan agreement including easy to answer questions to help generate a loan agreement for your unique purposes. Fill in the information on the loan agreement and bring to a notary to verify the signatures.

What is the easiest way to create a Loan Agreement?

Lucky you! The easiest way to create your customized loan agreement is right here on Form Pros! The answer is simple, it’s here on Form Pros! You can glide through the process worry-free and have your loan agreement in no time!

Why use our Loan Agreement generator?

Our easy to use loan agreement generator makes the process quick. Just have your loan information ready, enter it in when prompted, and your loan agreement is created and ready to use. It’s not worth the risk to overlook a loan agreement and fail to have one. Now, there is no excuse not to when you have Form Pros on your side customizing the way you do business.

Be sure to check out our budget-friendly subscription plan. You will have the ability to generate unlimited loan agreements tailored to your specific needs. Form Pros is your hub for forms just like this one, and many more!

Another form similar to a loan agreement, but a little less formal (usually between family), is a Promissory Note. We have that form ready for you as well; you can find it here!